Maximizing Your Disability Insurance Benefits: A Strategic Investment Approach

Experiencing a disability can be financially devastating without adequate protection. While Social Security Disability Insurance (SSDI) provides a safety net, strategic planning is essential to maximize your total benefits. Today about 80% of SSI recipients are eligible on the basis of disability. With the right plan that fits your specific situation, you can make sure you have enough financial support if you encounter a situation where you experience a disability.

This guide will give you the knowledge to take charge of your financial future.

The Wide-Reaching Financial Impact of Disability

Facing a disability can seriously affect how you handle your money in many ways. Here’s how:

- Lost Income: Most people rely on their jobs for money. But if you can’t work because of a disability, you stop getting your regular paycheck. The Social Security Administration says that about one out of every four 20-year-olds will have to stop working for at least 90 days because of a disability before they turn 67.

- Savings Drain: Without your income, your savings can disappear quickly, especially if you have to use them for everyday expenses. If your disability lasts a long time, it can become really hard to manage without some other source of money.

- Medical Bills: Disabilities often come with big medical bills. You might also need to spend money on things like home healthcare or special equipment.

- Money Problems: All this financial stress can make it tough to save money or invest. If you don’t have the right protection in place, you might even have to dip into your retirement savings early or sell your investments to pay for urgent expenses. Start opening any type of savings account to build a financial safety net. Prioritize saving to avoid tapping into retirement funds or selling investments during unexpected financial challenges.

Understanding how SSDI interacts with long-term disability, retirement benefits, passive income streams, and investing is key to optimizing your income sources. Working with experts like disability insurance attorneys can help create a tailored financial plan. Disabilities can have a big impact on your finances, and it’s important to plan ahead to make sure you have enough support if something like this happens.

The Pivotal Role of SSDI

To prevent complete financial ruin, Social Security Disability Insurance (SSDI) provides a crucial lifeline. SSDI is a government-run insurance program funded by payroll taxes that provides income replacement for severely disabled individuals expected to be unable to work for at least 12 months.

SSDI eligibility hinges on having earned sufficient work credits prior to becoming disabled. Benefits typically replace only a portion of prior earnings. For 2022, the average SSDI benefit is $1,358 per month.

So while SSDI offers a base level of income replacement, in most cases it is inadequate on its own to fully replace lost wages and keep pace with rising costs. Treating SSDI as the sole solution can leave dangerous gaps.

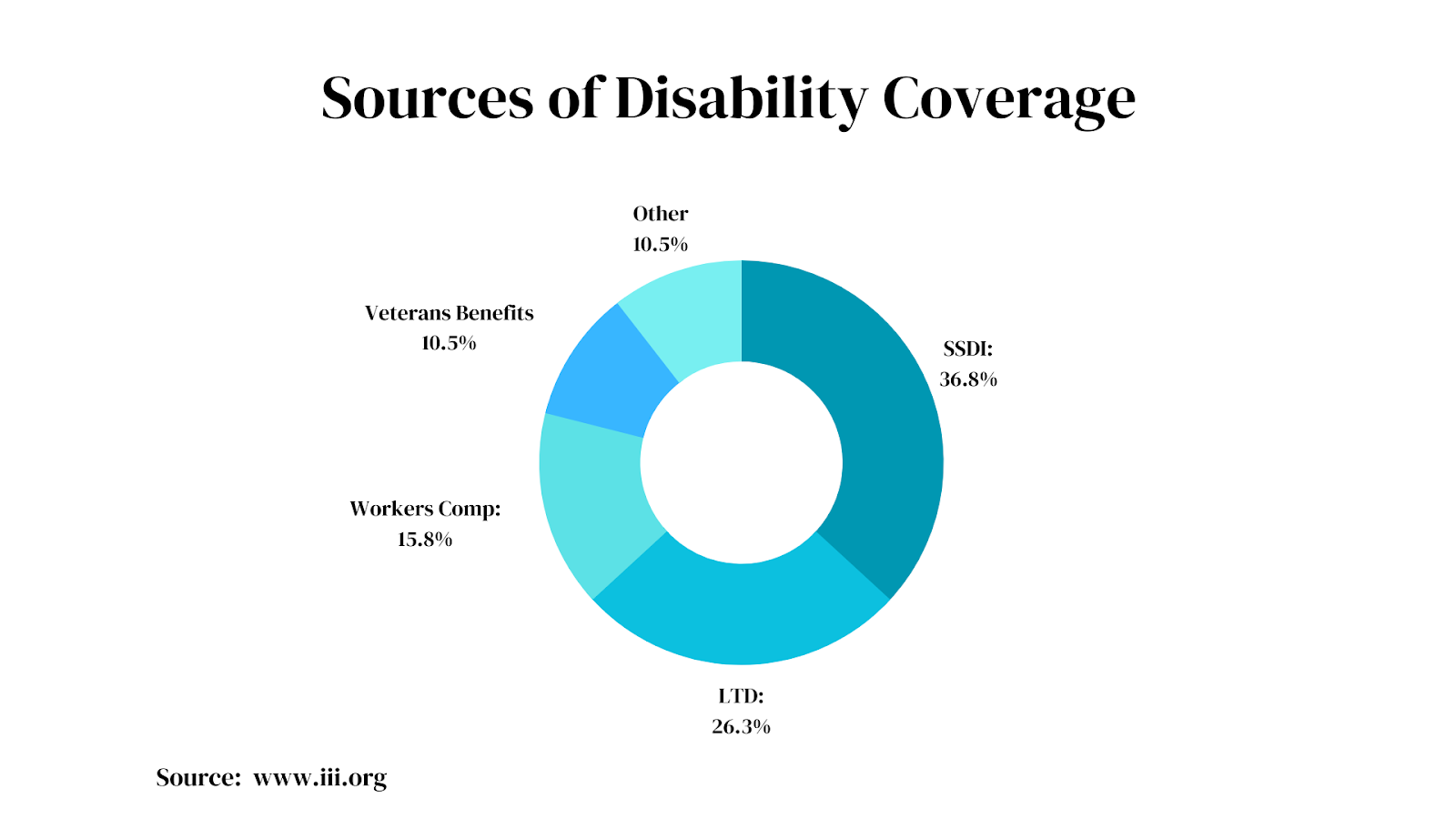

SSDI’s Connection to Other Benefits

Instead, SSDI should be viewed in the context of holistic disability financial planning. It intersects with other vital income sources, including:

- Long-term disability insurance – Private insurance that provides more generous benefits with more flexible eligibility.

- Retirement benefits – Social Security retirement benefits convert to SSDI if disabled before retirement age.

- Workers’ compensation – Provides wage replacement and medical care for job-related injuries/illnesses.

- Veterans’ benefits – Disability compensation for veterans with service-connected conditions.

- Passive income – Interest, investments, royalties, and rents can supplement SSDI.

With proper coordination across these avenues, the gaps left by SSDI can be minimized. However, it requires understanding how to harmonize SSDI with other benefits.

Distinguishing Social Security Disability Insurance From Long-Term Disability

One of the most complex interactions is between Social Security Disability Insurance and long-term disability insurance. Navigating between these two primary sources of disability income replacement is key for your financial security.

While both offer income replacement in case of disability, there are crucial differences:

SSDI

- Government-administered program

- Funded by payroll taxes

- Strict disability definition

- Requires work history/credits

- Provides on average $1,358/month

- Difficult to qualify for

- Benefits offset with work

Long-Term Disability Insurance

- Private disability insurance policy

- Paid for by individual

- More flexible disability criteria

- Less stringent work requirements

- Replaces 60-80% of income

- Higher acceptance rates

- Incentives to return to work

Understanding these key distinctions allows for smart coordination:

- Purchase adequate LTD coverage – Helps make up for SSDI’s low benefit amount and strict eligibility.

- Factor in offsets – LTD and SSDI offset, so increased LTD means lower SSDI dependence.

- Mind the definitions – LTD has more flexible criteria than SSDI’s stringent federal definition of disability.

- Work incentives – LTD encourages workforce reentry while SSDI severely limits working.

- Knowledge is power – An expert can help ensure your LTD and SSDI work in harmony.

With the right LTD policy, you can reduce over-reliance on SSDI, receive more adequate benefits, and gain more flexibility.

How Passive Income From Investments Impacts SSDI

Passive income streams are another area where coordination with SSDI is essential but often misunderstood. Passive income refers to earnings generated from investments and assets rather than active work. This includes:

- Interest from savings accounts or bonds

- Dividends from stocks

- Capital gains from selling investments

- Rental income from real estate

- Royalties from intellectual property

These income streams allow those with assets and investments to generate supplemental earnings. For the disabled, passive income could significantly help cover costs exceeding SSDI’s modest benefits. But how does this income impact your eligibility?

The good news is that when determining your SSDI eligibility and payment amounts, the Social Security Administration does not count:

- Income from stocks, bonds, or mutual funds

- Interest earned on your savings accounts or bonds

- Capital gains from selling your investments

- Income from rental properties you own

- Royalties from intellectual property

This means you remain fully entitled to your full SSDI benefits even with substantial investment holdings and passive income streams.

However, the bad news is that large one-time payments from selling investments could impact your eligibility for other need-based government programs. These include:

- Supplemental Security Income (SSI) – A program providing additional disability assistance for those with minimal assets/income. Substantial lump sums from selling investments could disqualify you.

- Medicaid and Medicare Savings Programs – These programs pay for medical costs and Medicare premiums based on your income/assets. Large investment sell-offs could push you above the limits.

- Subsidized Housing – These housing programs limit eligibility based on income and assets. Sudden large payments could jeopardize your qualifications.

The key is working with expert legal and financial advisors to structure your investments and strategically access funds in ways that maximize your income without compromising eligibility for other essential government benefits.

Employing a Comprehensive Strategy to Maximize Disability Benefits

Disability benefits were paid to over 9.2 million people. Simply optimizing your financial position in case of disability requires looking at the big picture across all potential income sources and thoughtfully coordinating between them.

With disability impacting so many aspects of your financial life simultaneously, adopting a siloed, piecemeal approach to benefits planning will leave you vulnerable.

The key is to work with specialized disability insurance attorneys and financial planners to develop an overarching strategy that integrates:

- Long-term disability insurance

- Social Security retirement and disability benefits

- Workers’ compensation

- Veterans’ benefits

- Passive income from investments

- Pension/retirement accounts

- Health savings accounts

- Life insurance conversion

By harmonizing these interconnected programs based on your unique situation, risks can be mitigated and benefits maximized.

This comprehensive approach should focus on optimizing aspects like:

- Timing of benefits claims and payments

- Accounting for offsets between programs

- Balancing savings and income streams

- Coordinating stay-at-work and return-to-work incentives

- Protecting eligibility across programs through smart asset management

- Ensuring adequate lifetime coverage as needs evolve

With this level of strategic planning, you gain the confidence that your finances will remain secure even in the face of serious disability.

FAQs

Can I receive both SSDI and Supplemental Security Income (SSI) benefits?

It is possible to concurrently receive both SSDI and SSI in certain situations. SSI is intended to supplement very low incomes, so if your SSDI monthly benefit is less than the maximum SSI amount, the two can complement each other up to that cap.

How long does it take to get approved for benefits after becoming disabled?

The process typically takes 3-5 months for initial determinations but can extend longer if appeals are required. Using a disability insurance attorney from the start can help expedite approvals. Proper documentation and clearly demonstrating how your disability prevents work are key.

Can my spouse or dependents receive benefits based on my disability?

Potentially, yes. Additional Social Security, Medicare, Medicaid, or VA benefits may be available for dependents. Spouses may qualify for benefits at age 62 based on their work history. Survivor benefits are also an option if your disability is terminal. Consult an expert on coordinating family benefits.

How do I determine the optimal level of long-term disability insurance coverage?

Your disability insurance attorneys and financial planners can help analyze your specific income needs in case of disability and identify an appropriate LTD policy and benefit amount. This factors in SSDI payments, existing assets, family status, healthcare costs, and more. Review your coverage annually.

Final Thoughts

Going through a serious injury or illness doesn’t have to ruin your finances if you plan well. But you need to think about how it affects all aspects of your money.

To protect your family’s financial future if something bad happens, you should combine Social Security Disability Insurance with other things like long-term disability, retirement benefits, and income from investments.

Start by learning about how all these programs work together. Then, get help from experts like disability insurance lawyers and financial planners to create a plan that’s just right for you and your family. This plan will make sure you have the best financial support if you ever become disabled.